👋 ASB Partners Nuggets 6.6.25

This is a short weekly email that covers a few things I’ve found interesting during the week.

Interesting Links/Reads

Many links are sourced from Marginal Revolution (bold and italics are my own to highlight what I found particularly interesting)

Despite Dalio’s guesstimate, knowing when doomsayers will be proven right is impossible. Consider Stein’s Law: “If something cannot go on forever, it will stop.” (Contrary to urban legend, that line wasn’t uttered by Ben Stein, who played the boring economics teacher in “Ferris Bueller’s Day Off,” but by his father, Herb, an actual economist.)

MICHAEL MAUBOUSSIN: "One of the hardest aspects of being a long-term investor is that even the best investments, or investment portfolios, suffer large drawdowns. A drawdown is the price decline from peak to trough. [Charlie] Munger not only argues that you have to be calm about these declines, he goes further to suggest that if you cannot deal with them “you deserve the mediocre result you are going to get.” In other words, big drawdowns are a price to pay for superior longterm investment returns... Long-term investors need to be aware of the pattern of drawdowns and be prepared to face them when they inevitably occur. The best investors and stocks suffer through large drawdowns, which can be considered a cost of doing business over the long haul. The median drawdown for the 6,500 stocks in our sample from 1985-2024 was 85 percent and took 2.5 years from peak to trough. More than one-half of all stocks never recover to their prior highs. Relative to smaller drawdowns, larger drawdowns, on average, take longer to occur, recover to the previous peak less often, and yet can provide attractive returns off the lows. Recoveries from drawdowns of all sizes have significant skewness, which means some stocks do extremely well relative to the pack. As a result, average returns from rebounds are higher than median returns. An investor who had the perfect foresight to create a portfolio of the stocks with the highest returns in the next five years would still see substantial drawdowns along the way. Indeed, one five-year stretch of the foresight portfolio had a 76 percent drawdown. This underscores how hard it is for professionals to manage through drawdowns."

From Matt Levine:

Limits to arbitrage

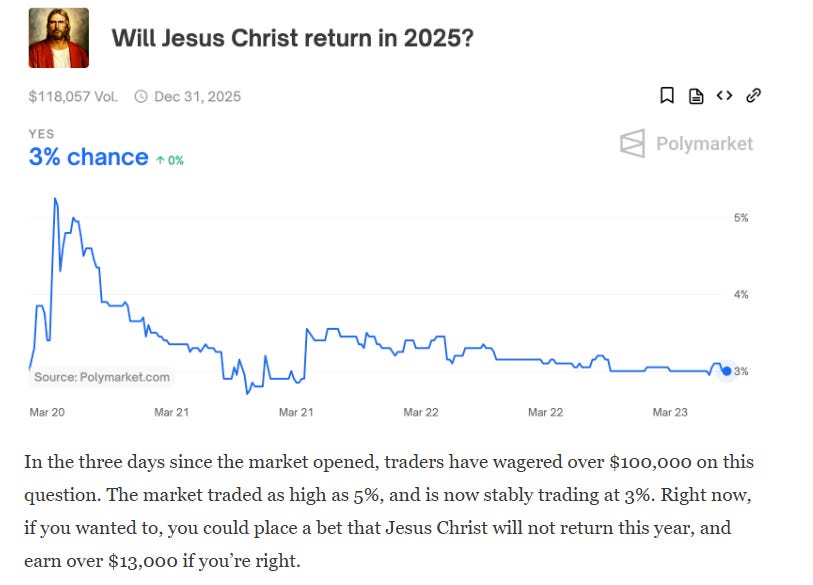

Here’s a fascinating post by Eric Neyman from March that has been making the rounds recently. Polymarket, the prediction market, lists a contract on “Will Jesus Christ return in 2025?” It trades today at what is conventionally called a “3% chance”: You can bet about 3 cents on “Yes” and get $1.00 on Dec. 31 if Christ returns, or you can bet about 97 cents on “No” and get $1.00 on Dec. 31 if he doesn’t.

Nothing in this newsletter is ever eschatological advice, but that 3% chance seems high. For one thing, over the last few centuries, the realized probability of Jesus Christ returning is considerably below 3% per year. Also, if Jesus Christ does return this year, are you really going to want to go to the online crypto prediction market to collect your gambling winnings?

So let’s say you think the actual probability is lower. Say you are completely confident that the actual probability of Christ returning this year is exactly 0%. How should you bet on that? What is the correct price of the No contract?

Well, the bet is that you put some money in now, and on Dec. 31, 2025, if you’re right, you get back $1. There’s a US Treasury bill that matures on Dec. 26, 2025, that has a yield of about 4.07%, meaning you can buy it for 97.7 cents today and get back $1 at the end of December. Surely you should not be willing to put more into a Polymarket bet today to get back $1 at the end of December. So 97 cents on the dollar — about a 5.2% yield — feels like a plausible price for this contract, if you’re sure you’re right.

That is a function of interest rates, though. In a world of zero or near-zero interest rates, you might pay 99 or 100 cents on the dollar; a dollar in seven months would be worth as much as a dollar now. In a world of very high interest rates, you might pay only 93 or 95 cents today for a dollar in seven months.

If 97 is the correct price to pay for the No contract, what is the correct price to pay for the Yes? Again, let’s assume that you are completely confident that the correct probability is zero. An intuitive answer would be “zero dollars”: There’s no reason to pay 3 cents today to get back 0 cents in seven months. But there is an important no-arbitrage condition, which is that the price of the No contract and the price of the Yes contract sort of have to add up to $1 (ignoring fees and bid/ask spreads). From Polymarket’s documentation: “Holding 1 ‘Yes’ share and 1 ‘No’ share is equivalent to having $1.00 (minus trading fees). As a result, Polymarket allows you to merge these shares back into USDC.” USDC is the Circle dollar stablecoin, and it seems fair to assume that it’s worth exactly a dollar.

And so if the No contract traded at $0.97 and the Yes contract traded at zero, then you could buy one No and one Yes for $0.97, combine them, and get back $1 immediately (not in seven months), which is 3 cents of free money. You’d do this until you arbitraged the Yes contract up to its correct price, which is $0.03.

One (dumb, but funny) way to put this is that the “Yes, Jesus Christ will return in 2025” contract is a bet on interest rates going up: If short-term interest rates went up to 8%, the No contract would be worth about $0.95, so the Yes contract would be worth about $0.05 and you’d make a 40% profit.

Another (somewhat less dumb) way to put this is that the Yes contract is a way to bet on Polymarket discount rates going up. Those discount rates are related to short-term risk-free US dollar interest rates, but they’re not the same thing. Neyman writes:

I hope you enjoyed it.

Adam