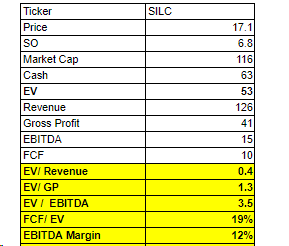

$SILC

~$17/stock with $24/share of Cash, Accounts Receivables, and Inventory and NO debt with an active buyback in place

Israeli stocks had a tough 2023. The 1-2-3 punch of higher interest rates, controversial judicial reform legislation, and finally the war in Gaza weighed on the broader indices relative to other markets globally:

This relative underperformance has created selected opportunities in Israeli stocks….Enter Silicom Ltd (SILC):

Silicom is a hardware manufacturer that makes networking and data infrastructure solutions. Designed primarily to improve performance and efficiency in Cloud and Data Center environments, Silicom’s solutions increase throughput, decrease latency, and boost the performance of servers and networking appliances

Silicom products are used by major Cloud players, service providers, telcos, and OEMs as components of their infrastructure offerings.

While it’s a relatively low gross margin business (low 30s), Silicom has consistently generated double-digit operating margins, and the business doesn’t have much CapEx (<$5mm/year). Design wins usually last 3-5 years which provides decent visibility.

Valuation TTM is not very demanding:

So how did we get here and what makes this compelling:

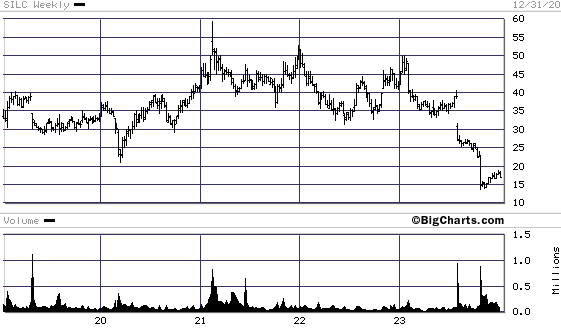

As mentioned above, it’s been a tough year for Israeli stocks and Silicom in particular. In addition to the 1-2-3 punch at the macro level, Silicom experienced a severe inventory correction in 2023, which means their suppliers over-ordered from 2020-2022 because of supply chain chaos relating to Covid, and they are now working off that inventory which hurt Silicom in 2023 and will continue to depress performance in 2024.

What’s the reason to be bullish in the long term? First, let’s start with the downside protection:

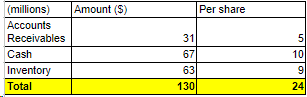

Even after the move off its lows in Nov.-Dec. 2023, Silicom still trades almost like a Ben Graham Net-Net:

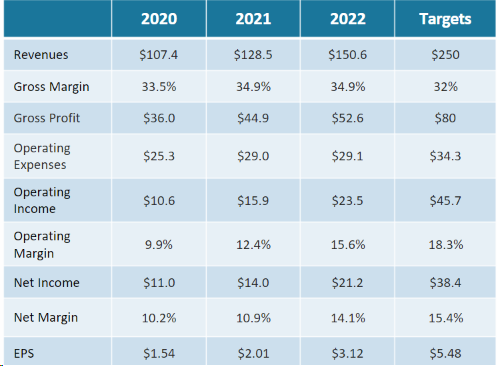

As relates to the upside, Silicom gave long-term guidance as recently as 2022 that they thought this business was capable of doing >$5/share in EPS over the medium term (not 3 years but probably more like 5 years):

I doubt management would bless that guidance now, but you have to appreciate that the stock now trades ~$17/share and they have >$9/share of cash!

On the Q323 conference call, they affirmed that they will continue to buy back their stocks:

While management has indicated that 2024 could be another challenging year, this business has had 18 years of continuous profitability and 22 consecutive quarters of on-track quarterly guidance (no misses). There’s a nice margin of safety and potential for a significant upside.